Pakistan’s real estate market has always had a deep financial and emotional connection with the Gulf. That connection is not limited to overseas jobs or family remittances. It also runs through investor psychology, Dubai property exposure, construction costs, and the wider belief that Gulf prosperity eventually supports buying power in Pakistan. That is why the question matters so much: if Dubai were hit much more severely and its property market actually collapsed, what would happen to Pakistan real estate?

The most likely answer is not a simple boom-or-bust story. It is a two-phase shock.

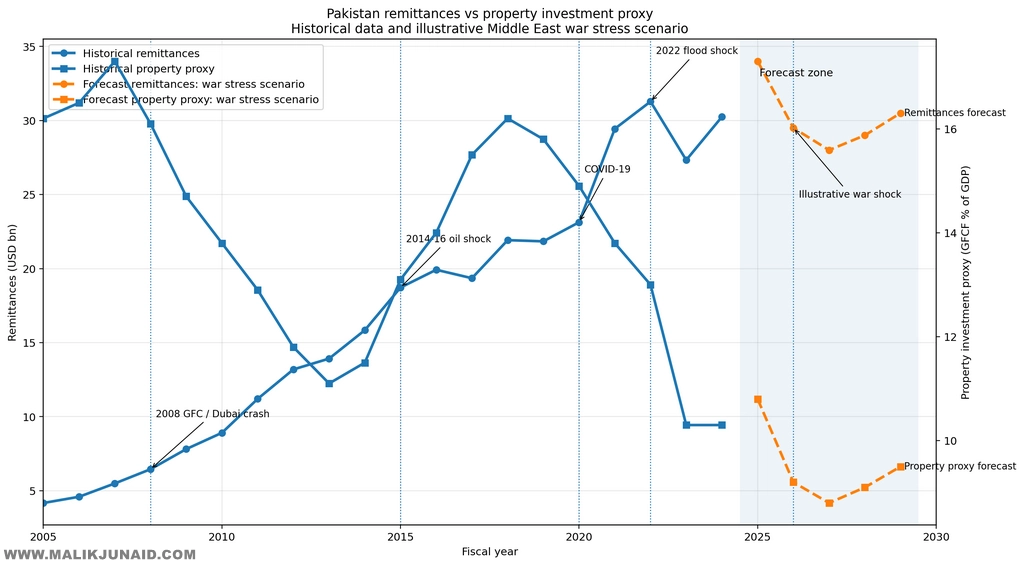

The first phase would probably be negative and fairly quick. Pakistan remains highly exposed to the Middle East through labor migration and remittances. A recent PIDE policy note says the Middle East contributes about 54% of Pakistan’s total remittances, hosts roughly 6 million Pakistani workers, and that a prolonged conflict could cut remittances by around $3–4 billion a year while also pushing more workers back home. Because remittances are one of the most important funding sources for household property buying in Pakistan, that would hit plot buying, mid-market residential demand, and under-construction projects that depend on steady installment inflows.

The second phase would likely be mixed, uneven, and highly location-specific. Pakistanis have also become major buyers in Dubai real estate. Reporting in February 2026 noted that Pakistan ranked as the second-largest source of investment in Dubai property in 2023, but had slipped to fourth place by 2025 as tensions rose. If Dubai prices fell sharply, some Pakistani investors would take direct wealth losses there, reducing their capacity to rotate capital into Lahore, Karachi, Islamabad, or Rawalpindi.

So the likely headline is straightforward: a Dubai collapse would probably hurt Pakistan real estate more than help it, at least initially. And if you are looking specifically at investor-heavy societies such as Faisal Town Phase 2, that initial damage could be more visible than in end-user dominated neighborhoods.

Why Pakistan Real Estate Is So Sensitive to the Gulf

A large portion of Pakistani property demand is not funded by mortgage depth or institutional capital. It is funded by family savings, overseas income, informal liquidity, and installment-based buying. That makes the market more vulnerable to sudden remittance pressure than many people realize.

Pakistan’s official remittance numbers underline that dependence. According to SBP’s FY24 annual report, workers’ remittances reached $30.25 billion in FY24, after $27.33 billion in FY23 and $31.28 billion in FY22. In the same broader macro picture, gross fixed capital formation has remained relatively weak, around 10.3% of GDP in FY24, which is one reason why any external cash shock can affect property more than it would in a deeper, more diversified investment market.

That matters because Pakistan property is not one market. It is a mix of very different segments:

speculative files and early-stage plots, premium investor-led apartments, mid-market family housing, and genuine end-user homes in prime urban locations. A Gulf shock does not hit all of these equally.

The most immediate pressure would fall on:

- speculative plots and files,

- mid-income residential demand dependent on overseas cash,

- under-construction schemes that rely on monthly installment discipline.

By contrast, end-user housing in strong urban locations usually proves more resilient because people still need places to live, and salaried demand does not disappear as fast as investor sentiment.

What Happens First if Dubai Is Hit Hard?

The first impact would most likely be weaker demand before any supposed “opportunity inflow” appears.

A common market assumption is that if Dubai becomes risky, money will automatically leave Dubai and come into Pakistan property. That sounds logical on the surface, but history suggests it is too optimistic. When investors are frightened by war, infrastructure risk, and capital loss, they often move first into cash, dollars, gold, or safer jurisdictions rather than into a market like Pakistan that already has documentation friction, uneven tax enforcement, slower resale liquidity, and development uncertainty.

That means the near-term impact would probably be:

- fewer new buyers,

- slower resale turnover,

- lower speculative appetite,

- more “urgent sale” inventory,

- greater pressure on developers’ cash flow.

This risk is no longer theoretical. Reuters reported on March 20, 2026 that the Dubai property sector was already showing early signs of weakness amid escalating regional tensions. According to the report, UAE real estate transactions fell sharply in early March, some high-profile properties were being offered at 12–15% discounts, and analysts warned that population growth and pricing could come under pressure if conflict persisted. Reuters also noted that the wider conflict had disrupted perceptions of Dubai as a safe haven.

If Dubai weakens while oil and shipping costs rise, Pakistan real estate faces a double squeeze: demand softens while construction costs rise.

Why Construction Costs Could Become a Second Shock

Even if a buyer wants to hold through volatility, developers still need cement, steel, transport, diesel, logistics, and working capital. A Middle East war that affects energy infrastructure or the Strait of Hormuz can push those costs higher. Reuters and AP both reported in March 2026 that the conflict had sharply lifted oil prices and disrupted Gulf shipping and energy flows, increasing the economic risks well beyond the battlefield itself.

For Pakistan property, that means:

- slower development on ground,

- higher construction costs,

- more pressure on installment-based projects,

- weaker margins for builders and developers,

- delayed possession timelines in vulnerable schemes.

This is where investor-heavy and development-stage projects become especially exposed.

Karachi, Lahore, Islamabad: The Impact Would Not Be Uniform

A Dubai property collapse would not affect every Pakistani city in the same way.

Karachi could feel the strongest immediate sentiment shock because of its business culture, Gulf-connected investor base, and long-standing financial ties to overseas capital. Investor hesitation there often spreads quickly through commercial and residential segments.

Lahore could see slower speculation in files and plots, particularly in projects where price momentum depends more on buyer expectations than immediate construction delivery.

Islamabad and Rawalpindi may have some cushion because of local salaried demand, government-linked employment, and stronger end-user interest in selected sectors. But overseas-driven pockets would still soften, especially where investors dominate resale activity.

In short: the same external shock would likely produce different price behavior in different cities, and even sharper variation within the same city.

What History Tells Us: Four Useful Examples

No historical event perfectly matches a hypothetical Dubai collapse during a larger regional war. But Pakistan has already lived through several useful “mini-experiments” that show how property reacts to Gulf stress, remittance shifts, and confidence shocks.

1. The 2008 Global Financial Crisis and Dubai Property Crash

Dubai’s real estate market was hit brutally in 2008–09, with large price declines, project cancellations, and layoffs among expatriates. Pakistan did not see a property boom from that crash. Instead, it saw stress, slower momentum, and weaker confidence. Research reviewing the effects of the global and Gulf financial crises on Pakistan found that investment from the UAE and other Gulf countries fell sharply after the crisis, while migration and remittance patterns also came under pressure.

The lesson is important: a Dubai crash did not automatically redirect wealth into Pakistan property. It created short-term stress first.

2. The 2014–2016 Oil Price Crash

When oil prices collapsed, Gulf economies slowed, hiring softened, and overseas workers faced more uncertainty. Pakistan did not experience a dramatic real estate crash, but plot markets cooled and liquidity tightened. End-user demand held up better than speculative activity. Historical analysis of Pakistan’s exposure to Gulf crises points to reduced migration momentum and investment weakness following the oil shock years.

The takeaway: when Gulf income weakens, Pakistan real estate usually loses fuel rather than gaining a new inflow.

3. COVID-19 and the 2020–2022 Property Boom

COVID looked like it should have produced a remittance collapse, but Pakistan saw the opposite. Formal remittance channels strengthened, restrictions redirected transfers through official systems, and local policy settings supported risk-taking. The result was a major property boom across Lahore, Karachi, and Islamabad. That period is one of the clearest proofs that if remittances remain strong, Pakistan real estate can rise even during global turmoil.

This is the positive counterexample, and it proves something crucial: the direction of Pakistan property depends less on fear headlines alone and more on what actually happens to overseas inflows and domestic policy.

4. Gulf Tensions in 2023–2026

The more recent pattern is especially relevant because Pakistanis are now more exposed to Dubai than they were in 2008. Dawn reported that Pakistan was a top source of Dubai real estate investment in 2023, but that ranking slipped by 2025 as tensions rose and investors became more cautious. That suggests that a new Dubai downturn would hit not only income channels through remittances, but also wealth channels through direct property losses.

That is the major twist compared with older episodes: today, many more Pakistanis have direct exposure to Dubai property cycles.

What This Means for Faisal Town Phase 2

When we bring this macro view down to a project level, Faisal Town Phase 2 stands out as a useful case study. It sits in a part of the market that often attracts investors looking for medium-term appreciation, development-led momentum, and installment-driven entry. Those features can be strengths during a bullish cycle, but they can become vulnerabilities during an external shock.

Under a severe Middle East war scenario, Faisal Town Phase 2 would likely face three linked pressures.

First, buyer demand could weaken quickly, especially from overseas or speculative buyers. In projects where files and early-stage plots are a major part of activity, lower confidence usually shows up first in lower turnover.

Second, development cash flow could come under stress if installment discipline weakens and construction input costs rise at the same time.

Third, urgent-sale inventory could increase, particularly among short-term holders who entered for quick appreciation rather than long-term building plans.

That does not mean every part of the project would collapse equally. In most Pakistani property cycles, the biggest early hit is usually taken by speculative layers of the market. Genuine end-users, long-term holders, and buyers with stronger liquidity are normally more patient.

So for Faisal Town Phase 2, the most likely pattern is:

- files and short-term flipping positions are most vulnerable,

- resale plots face pressure but usually more gradually,

- serious end-user interest is more resilient,

- recovery, when it comes, tends to begin after weaker hands exit.

For readers who want on-ground project updates or direct comparison material, it is contextually useful to review Faisal Town Phase 2 and broader investment commentary at MalikJunaid.com, especially when comparing location, access, and market positioning across nearby schemes.

Could Any Part of Pakistan Property Benefit?

Yes, but probably later and only selectively.

Once the initial panic phase passes, some capital may search for discounted opportunities inside Pakistan. But based on history, that returning capital usually does not fully offset the damage caused by weaker remittances, lower confidence, and macro pressure on the rupee.

A more realistic medium-term outcome would be:

- stabilization after the first shock,

- selective bottom-fishing in strong projects,

- resilience in prime end-user housing,

- slower and more uneven recovery than many speculators expect.

That is why the best summary is still this: near term bearish, medium term mixed.

Practical Conclusion

If Dubai were hit severely and its property market actually collapsed, Pakistan real estate would probably face a clear first-round negative effect. Demand would weaken before any opportunity narrative took hold. Speculative files and plots would likely be hit hardest. Luxury investor-driven segments would be vulnerable. End-user housing in stronger urban areas would be more resilient. And projects that depend heavily on installment inflows could feel the squeeze from both weaker buyers and higher construction costs.

History does not support the easy myth that “Dubai crash means Pakistan boom.” The past shows the opposite pattern more often: Gulf stress tends to slow Pakistan real estate first, and only later create selective opportunities if remittances recover and local policy becomes supportive.

For buyers, sellers, and investors trying to navigate this kind of volatility, project-level due diligence matters more than ever. If you want professional guidance on Faisal Town Phase 2, Capital Smart City, or broader Islamabad-Rawalpindi opportunities, you can contact Gains Real Estate and Marketing Pvt Ltd through 03331003535 or 03355592930. For WhatsApp, use WhatsApp 03331003535 or WhatsApp 03355592930 where direct, fast project discussion is actually helpful. For related project research and comparisons, contextually relevant resources include Capital Smart City, Capital Smart City Phase 3, and Capital Smart City Islamabad.